Difference Between Term And Whole Life Insurance In India

The Cost Factor Unveiled

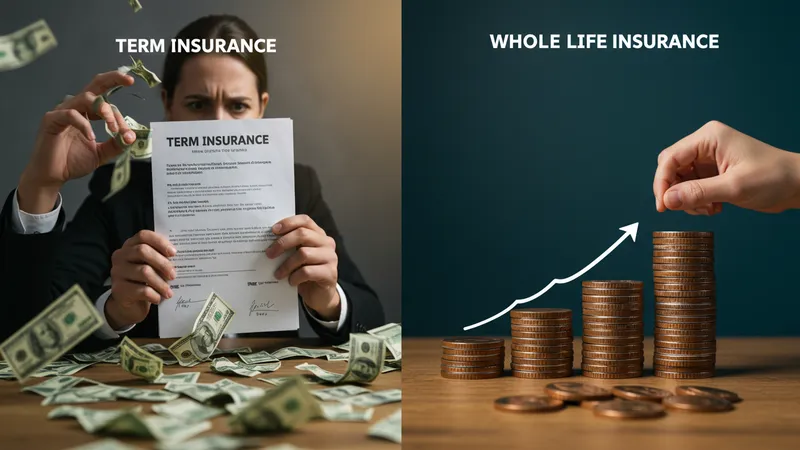

Let’s delve into the real cost of term insurance. While the upfront premium might seem budget-friendly, it often comes with hidden penalties. Miss a single payment, and your entire plan might get nullified. You won’t just lose coverage; you might end up paying double to restart a new plan. This hidden pitfall isn’t something agents proudly highlight, often leaving consumers in the lurch. But there’s one more twist that will make you rethink the term insurance as a cost-effective option…

Whole Life Insurance, with its high costs, sounds daunting, doesn’t it? Interestingly, it includes a savings component that builds over time. This means you’re not just paying for a safety net. However, it’s essential to realize those savings don’t always stack up as quickly as you might hope. Unforeseen charges and fluctuating interest rates could slow the growth, making it less beneficial than it sounds. What you read next might change how you see whole life policies forever.

The term versus whole life insurance debate centers around uncertainty. Both are riddled with perplexing fine print, and since many Indian policies follow unique regulations, the complexity escalates. Without a specialized advisor, navigating these waters can seem impossible. But there’s one insider tip that might simplify your decision…

For many Indians, cultural norms gravitate towards long-term security, often leaning towards whole life insurance. Despite higher premiums, people bank on lifelong coverage due to the persistent uncertainty. Yet, an emerging trend is shifting perspectives, with an unexpected insurance strategy capturing attention. Stay tuned for this game-changer that could revolutionize your approach to coverage…